※ This article is for informational purposes and personal analysis only, not a recommendation to buy or sell any specific investment products. Please verify with official sources and consult qualified professionals for investment, tax, or legal advice; you are solely responsible for your decisions. Market conditions may change after the time of writing.

Foreword

For a while, there was an investment trend led by retail investors focusing heavily on US overseas stocks. Now, a new term has become trendy: “Ilhak Ants” (retail investors focusing on Japanese stocks). Unlike the expectations of many, the real estate market prices in major Japanese hub cities are trending upward. Just like stocks, you can invest in the Japanese real estate market via J-REITs. In this post, we will explore what J-REITs are, their advantages, and major REIT products.

1. What is J-REIT Investment?

Japan’s Real Estate Investment Trusts (REITs) are similar to those in the US, with major Japanese corporations participating in the market. As of 2023, there are 41 REIT funds in Japan, forming the largest real estate investment trust fund market in Asia. On a global scale, it ranks second only behind the United States.

In 2000, the Japanese government amended the “Investment Trust Act” into the “Act on Investment Trusts and Investment Corporations,” allowing the funds raised by investment trusts to be used for real estate investments. This established the legal status of real estate investment trusts in Japan.

The major REITs listed on the Tokyo Stock Exchange include:

- Nippon Building Fund (NBF) REIT Inc.

- Japan Real Estate Investment Trust (JRE)

- Nippon Prologis REIT Inc.

- Nomura Real Estate Master Fund REIT

These REITs encompass various sectors including office buildings, retail, logistics, and residential real estate. The performance of these REITs can be tracked on portals such as JAPAN-REIT.COM and J-REIT.jp.

2. What are the advantages of investing in J-REITs?

Investing in Japanese Real Estate Investment Trusts (REITs) presents several benefits:

- Market Accessibility: REITs allow investors to access a diverse portfolio of real estate assets that might be difficult to achieve through direct property ownership.

- Liquidity: Unlike physical real estate, REITs are traded on the stock exchange and can be bought or sold at any time, providing investors with ultimate liquidity.

- Alternative to Property Ownership: REITs offer a way to invest in real estate without the burden of managing the property or paying direct property taxes.

- High Dividend Yield: Generally, REITs offer high dividend yields, which can provide investors with a stable income stream.

- Low Minimum Capital Requirement: Investing in REITs requires relatively low capital input, making them accessible to a broad spectrum of investors.

The fact that there is a strong ally named the Bank of Japan (BOJ) elevates the attractiveness of investing in J-REITs. The BOJ has been increasing its investment scale in listed stocks. Even during the crisis of the COVID-19 pandemic in 2020, they expanded their REIT purchasing scale. Considering the abysmal interest rates of Japanese government bonds, it is highly likely that the BOJ’s scale of investment in listed stocks and REITs will continue to grow.

A characteristic advantage of J-REITs is the system allowing “negative goodwill” to be excluded from distributable profits. For instance, if REIT ‘A’ acquires REIT ‘B’ cheaply—say REIT B is worth 60 billion KRW but is acquired for 50 billion KRW—a negative goodwill of 10 billion KRW is generated. While REITs are generally required to distribute their earnings as dividends, that 10 billion KRW can be retained without being paid out. These resources can then be utilized during crisis situations when paying dividends becomes difficult. Ultimately, this equates to providing considerable stability to REITs.

3. How to invest in J-REITs?

One method is investing in individual REITs. Since REITs are traded on the stock market, just like trading US stocks, investing in J-REITs means investing directly in the Japanese market. The currency used is obviously the Japanese Yen since it is the Japanese market. For stability, one should consider the market’s representative individual REITs as investment targets. If you are not familiar with overseas stock investments, choosing a public mutual fund is another viable option.

However, personally, since the Yen exchange rate is currently at a historic low, I recommend considering individual REIT investments, keeping future foreign exchange gains in perspective. The representative REITs are listed below. All these REITs track the TSE (Tokyo Stock Exchange) REIT Index. The data below is taken from http://www.japan-reit.com. Although it is in Japanese, the crucial part is the 4-digit code (ticker) at the front, which allows you to check significant information in English on sites like investing.com. Checking key data through that ticker allows you to invest in J-REITs using the same method as trading overseas stocks.

Source: reference screenshot adapted from japan-reit.com.

Editorial note: screenshots in this post are archival references and may not match current UI or latest figures. For current numbers, use the linked official pages first.

4. Expected Returns and the Tangible Warmth in the Asset Market

While average dividend yields hovered over 4% back in 2023, the explosive surge in prime real estate asset values in central Tokyo has slightly compressed these apparent yields recently. Conversely, this is hard proof that the ‘Capital Gains’ of the underlying assets are rising fiercely.

Currently in 2026, the BOJ has raised the policy rate to 0.75 percent and the 10-year JGB yield has risen to approximately 2.43 percent—compressing the yield spread between J-REITs and government bonds to roughly 200–250 basis points. Risk sentiment around Japanese assets remains constructive on the real-estate fundamental side (vacancy at multi-year lows, record inbound tourism), but the financing environment is the tightest it has been since before the ZIRP era. Rather than assuming a one-way cycle, I treat this as a scenario exercise where cash-flow resilience and refinancing quality matter as much as momentum.

4.1 A simple scenario worksheet (illustrative)

| Case | Distribution yield | FX move (JPY vs KRW) | Price move | Back-of-envelope total |

|---|---|---|---|---|

| Defensive | 3.2% | -3.0% | -2.0% | about -1.8% |

| Base | 3.6% | 0.0% | +2.0% | about +5.6% |

| Upside | 3.8% | +4.0% | +6.0% | about +13.8% |

This is not a forecast. It is a transparency template so readers can challenge each assumption before they allocate capital.

4.2 My own scenario chart (illustrative SVG)

Method note: each bar is the arithmetic sum of the scenario inputs shown above. This chart is an educational worksheet, not a performance promise.

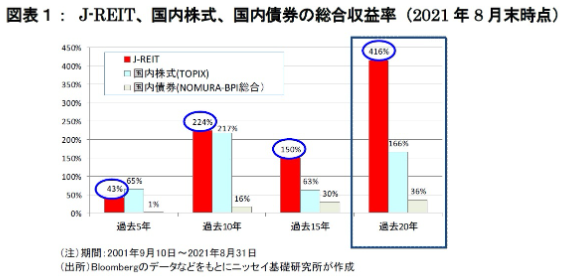

According to research conducted by the Nissei Basic Research Institute, as of late August 2021, the REIT return rate over the past 20 years was 416% (annualized at about 8.6%), which is quite respectable. During the same period, the Japanese stock market, represented by TOPIX, rose by only 166%. This is data proving that the true potential of REITs simply cannot be ignored. Over the past 5 years, the return is 43%. While it is lower than TOPIX over the shorter term, considering the robust stability of dividends, its attractiveness has certainly not diminished.

Those investing in J-REITs can factor in factors like stable dividends of around 3~4%, the possibility of future foreign exchange gains, and capital margins through potential market value increments. Projecting a definitively guaranteed return is impossible for any investment. However, from the standpoint of “stability,” I believe J-REITs are an overseas investment that holds significant advantages.

Source: reference chart adapted from public quote data on investing.com.

5. Looking at the Top 3 J-REITs

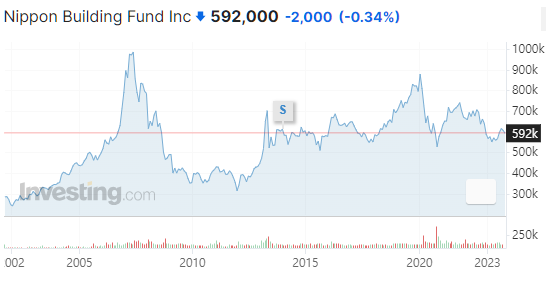

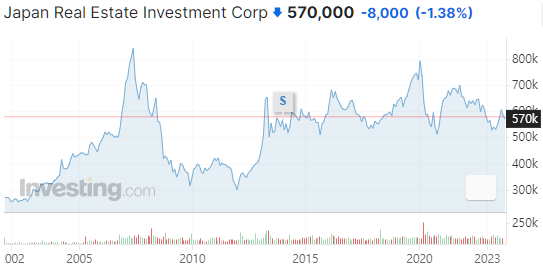

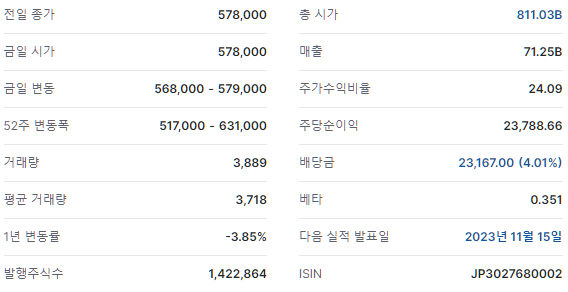

As of the end of September 2023, the total market capitalization of all J-REITs surpassed 15.7 trillion Yen. Even factoring in the weak Yen, it equates to a scale of roughly 140 trillion KRW. Looking at the top 3 REITs by market capitalization, we have the following. You can look up detailed information using the ticker symbols in the parentheses. I’ve compiled simple charts and general info from investing.com below. Please refer to them.

- Nippon Building Fund Inc (8951): Historically one of the largest J-REIT names by market value.

- Japan Real Estate Investment Corp (8952): A core office-heavy vehicle often used as a market bellwether.

- Nomura Real Estate Master Fund Inc (3462): A diversified platform with recurring institutional attention.

- Japan Retail Fund Investment Corp (8953): Smaller than the largest two, but frequently discussed for income sensitivity.

Data freshness note

Several numeric examples in this article are historical snapshots (mainly 2023 references) preserved for context. As of April 2026, the BOJ policy rate stands at 0.75 %, the 10-year JGB yield is approximately 2.43 %, and the TSE REIT Index is at roughly 1,916 points. Before making any decision, verify the latest monthly disclosures on J-REIT.jp and Japan REIT, then cross-check policy context with BOJ statistics.

Source: investing.com ticker 8951 (reference screenshot).

Source: investing.com ticker 8952 (reference screenshot).

Source: investing.com ticker 8953 (reference screenshot).

Source: investing.com ticker 3462 (reference screenshot).

Conclusion

“In 2020, while many global REITs struggled to maintain distributions, several J-REITs proved more resilient than expected. That does not guarantee future returns, but it shows why income-focused investors keep this market on the watchlist. The J-REITs introduced here are largely backed by commercial assets in major Japanese urban centers. If you hold a constructive long-term view on central Tokyo leasing and redevelopment, J-REITs can be a practical way to gain listed exposure to that thesis.

Further reading in this series

- 3 Things to Know About Real Estate Investment in Japan

- Hotel REITs vs Office REITs: Which Recovered More After COVID?

- Japan Rate-Hike Cycles and J-REITs: Three Historical Lessons

Investor Action: Session Summary & Check

- NAV: Check if the current price is at a discount to Net Asset Value (P/NAV < 1) to ensure a margin of safety.

- LTV: Audit individual REIT financial statements to ensure LTV is stable at the 40-50% level.

- Sectors: Review the weight of logistics or hotel sectors that can pass on inflation through rent increases.

Disclaimer: This article is for informational and educational purposes only and does not constitute investment advice, legal counsel, or tax guidance. Always consult a licensed professional before making any financial decisions. Past performance is not indicative of future results.